2017 Recession?

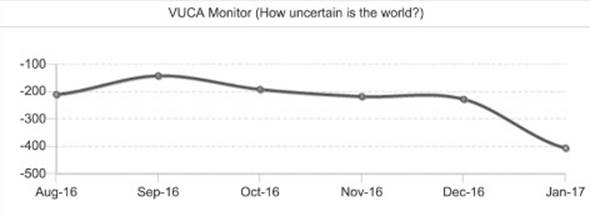

Athena is reporting a significant downturn in global feelings of uncertainty in past 6 months. Similarly, the pundits seem less sure of continued stability. Are these the early signs of a looming recession? The risk of either a US or global recession in 2017 is no more than 25%. But it’s our opinion that the odds of a recession could be increasing and there’s a need for vigilance.

What is changing?

- The global economy remains highly vulnerable to adverse shocks with market turbulence, oil price crash, weak commodity prices & continued geo-political conflict as key threats & risk factors.

- The outlook for global GDP growth has again deteriorated and risks have increased considerably.

- In 2017, growth will remain fragile and below +3% for the sixth year in a row.

- The risk of a recession gets marginally more difficult to avoid by the fall of 2018.

- Global growth will muddle along and the U.S. will not fall into a recession.

- A potential trade war triggered by Trump is the top risk to the global economy over the next two years.

- Britain will get through the immediate financial turbulence and a possible recession just fine.

- UK Consumers are going to face lower wages and higher prices next year following the slump in the value of sterling.

- UK consumer spending growth is projected to remain stronger than overall GDP growth at around 2.9% in 2016 and 2.2% in 2017.

- Shrinking energy consumption per capita puts the world (or individual countries in the world) at the risk of recession.

- In 2017 Russia's output will enter a zone of positive growth rates.

- Countries with close links to Russia are expected to continue feeling the trade impact from the current Russian recession as well as from the extended sanctions against Russia (and counter - sanctions against the EU).

- China will run into a debt crisis in either local government debt or corporate debt.

- Political instability has the potential to further set back Brazil's expected economic recovery from its deep recession.

- Japan's economy has dodged a recession after it grew faster than expected in the first three months of the year.

- Geopolitical risks remain high particularly with respect to the conflicts in parts of Ukraine and in the MENA region.

- Sub-saharan African growth is expected to pick up modestly to 2.9 per cent in 2017 as the region continues to adjust to lower commodity prices.

- The growth of Europe's auto market is expected to slow considerably this year after three consecutive years of strong gains.

- Fundamentals in Europe are weak and a crisis of confidence will send Europe to the similar path of the U.S.

- The IMF forecasts Venezuela will be in recession until at least 2019.

- Nigeria will get out of recession and grow its Gross Domestic Product by one per cent in 2017.

- Turkey depends on international investors to help finance a current-account deficit that will widen to almost 5 percent of output next year.

- Growth in Turkey is projected to moderate to around 3 per cent in 2017 on lower expected private investments owing to higher wage bill costs and the country credit rating downgrade as well as sustained weakness of the outlook for tourist arrivals.

- In the Pacific, growth for 2016 is expected to moderate to 3.9% in 2016 from 7.1% in 2015.

Implications

- A trade war could put the U.S. and global economies into recession.

- With rates below 0.5 percent and on track to rise very slowly, any small shock in the next few years could cause major economic damage.

- Insipid wage growth could still convince the US Federal Reserve to adopt caution by not implementing any further rate hikes until next year.

- Japan may opt to forgo a rate hike rather than risk sending the economy into recession.

- Sub-Saharan Africa countries (SSA) with high debt servicing costs (such as Mozambique and Angola) will be severely impacted by a global downturn in economic growth.

- Scuttling NAFTA or imposing a massive border tariff could lead to U.S. job losses and could cause automakers to move to other low-cost countries for vehicle production rather than building new plants in the U.S.

- The IMF is forecasting that Italy could be in recession for two decades.

- Sanctions relief would help Russia to return to the state of economic stagnation that prevailed before the Ukraine crisis when annual growth had already slumped to 1.3 per cent.

Sentiment Analysis

Forecast:

Insight: