Water-Energy-Minerals Nexus: A Weak Signal of Resource Scarcity Disruption

The intensifying interdependence between critical mineral extraction and freshwater scarcity marks a weak signal with potential to reshape global capital allocation, regulatory frameworks, and industrial design in resource-critical sectors. This underexplored nexus could alter supply chain resilience strategies and transform governance of natural resources over the next two decades.

While critical minerals demand surges amid climate and geopolitical volatility, the associated water stress embedded in extraction processes remains insufficiently addressed. Emerging efforts in large-scale water-saving agricultural technologies and localized mineral production hint at an inflection where water availability will become an equally, if not more, binding constraint than mineral reserves alone. This development is structurally relevant as it may redefine how industries prioritize investment, with implications spanning energy, manufacturing, and food security systems globally.

Signal Identification

This signal qualifies as an emerging inflection indicator because rising demand for critical minerals coincides with intensifying, localized water scarcity risks—a linkage currently underappreciated in strategic resource planning. Water stress is already quantifiable globally but remains peripheral in mineral supply chain risk assessments, suggesting a nascent but growing recognition that water and minerals cannot be decoupled in sustainable sourcing. The plausible time horizon for this dynamic to materially influence capital allocation and policy is medium to long term, approximately 10–20 years, with a high plausibility band given convergent climate, hydrological, and demand trends. Affected sectors include mining, energy production, agriculture, and water infrastructure.

What Is Changing

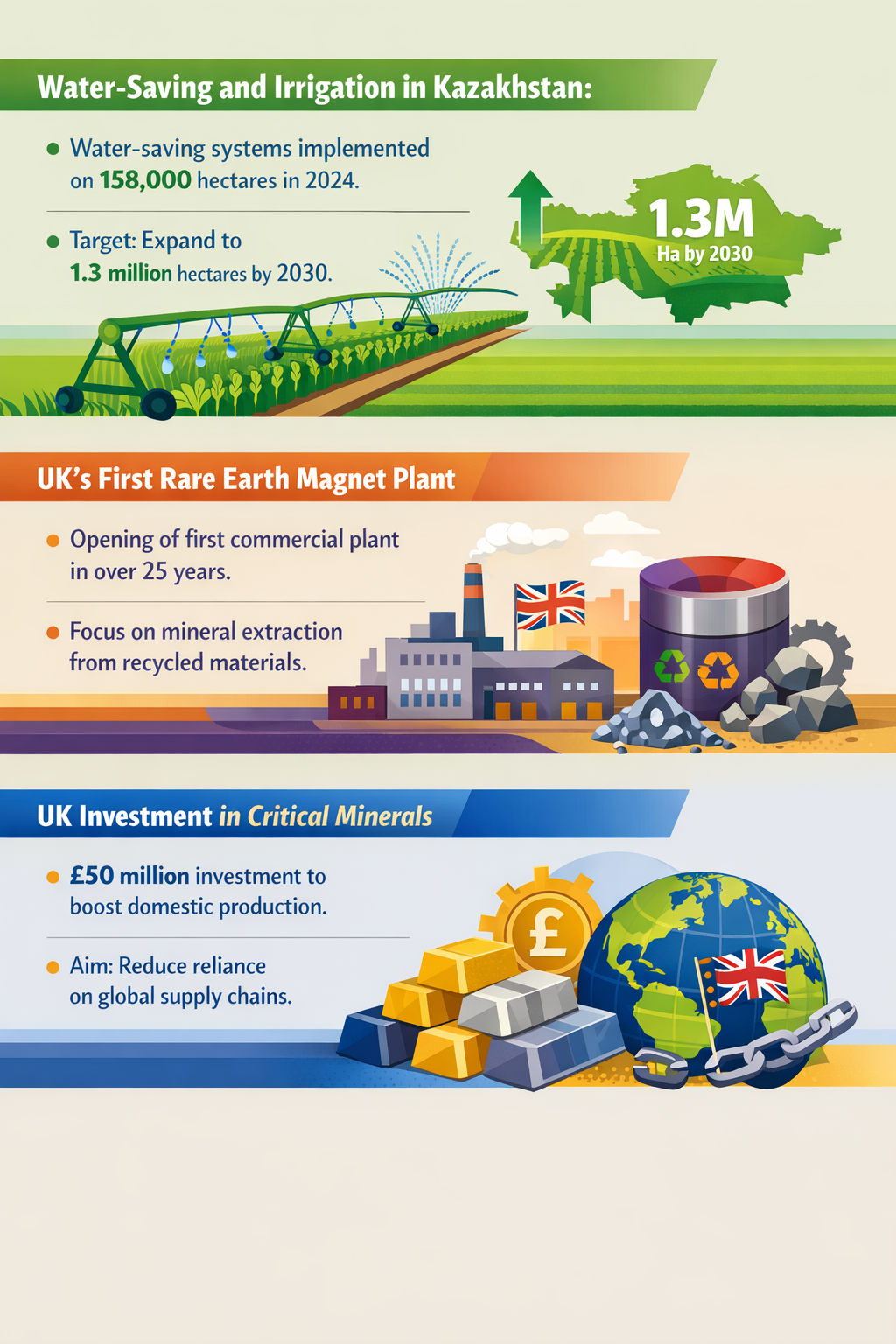

Global energy and defense sectors anticipate critical minerals demand to quadruple by 2040, driven by clean energy transitions and technological evolution (ORF Online 04/03/2026). Supply chain resilience strategies prioritize diversifying mineral sources, including investing in domestic production hubs like the UK’s £50 million push for local critical mineral mining (Emperor Works 02/07/2026).

Simultaneously, water scarcity is intensifying with measurable global drought conditions raising risk exposure for extractive and agricultural operations alike (ClimateCheck 11/01/2026). For example, Kazakhstan’s large-scale rollout of water-saving irrigation on 158,000 hectares in 2024—targeting 1.3 million hectares by 2030—illustrates how water efficiency technologies are transitioning from experimentation to mainstream adoption (Trade.gov 15/11/2025).

This geographically specific water stress implicates mining, notably in regions like Africa where governments and stakeholders aim to capture more value from critical minerals through integrated extraction-to-value pipelines (SAIMM 23/02/2026). Yet water resource management is notably absent from these discussions at scale. The systemic oversight of water embedded in critical mineral supply chains signals a blurring boundary between mineral scarcity and hydrological limits.

The recurring structural theme is that water availability is converging as a critical, yet under-recognized, constraint that could escalate risk profiles, raise operational costs, and call for new industrial ecosystem designs that integrate water stewardship explicitly into mineral sourcing and processing.

Disruption Pathway

As demand for critical minerals accelerates, extraction in water-stressed regions is likely to catalyze increased regulatory scrutiny and social license challenges linked to water use conflicts. This could increase the cost of capital and operational permits for projects failing to incorporate water-saving technologies or fail transparent resource risk disclosures.

Concurrently, advancements and subsidies for water-efficient technologies, as seen in Kazakhstan’s irrigation reforms, demonstrate conditions that could accelerate water stewardship adoption in mining and adjacent sectors. Investors and governments may impose water use intensity metrics as part of ESG (Environmental, Social, and Governance) frameworks, creating new industry norms.

As these dynamics unfold, mining companies and governments may adapt by integrating water resource management into critical mineral extraction strategies, potentially shifting cluster locations toward less water-stressed geographies or incentivizing circular water use and recycling innovations.

This feedback loop may incentivize cross-sector collaboration—linking water infrastructure, energy, and mineral supply chains—prompting regulatory frameworks that treat water and minerals holistically rather than in silos. Conversely, failure to adapt could lead to bottlenecks or stranded assets, especially where water scarcity precipitates community conflicts or ecosystem degradation.

Over time, dominant industrial models may shift from raw extraction-focused to resource nexus-informed ecosystem models incorporating polycentric governance that accounts for water-mineral interdependencies, elevating water as a first-order strategic resource inseparable from mineral capital planning.

Why This Matters

The decision relevance is high for regulators, investors, and industrial strategists who must anticipate not only mineral availability but also the freshwater footprint embedded in supply chains. This signal may recalibrate investment toward jurisdictions and technologies offering more integrated water-mineral risk mitigation, thereby impacting capital flows.

Regulatory bodies could evolve frameworks mandating transparent water risk disclosure linked to mineral extraction, affecting project approvals and financial liability for environmental impact. For industrial actors, competitive positioning will hinge on water stewardship innovation as climate change intensifies stress on hydrological systems.

Supply chains currently assessed predominantly on geopolitical and material criteria might shift to include embedded water scarcity, compelling new sourcing strategies aligned with sustainability and resilience. These shifts may also reframe liability regimes where water impacts become a trigger for compensation or remediation obligations, introducing nuanced governance challenges.

Implications

The water-critical minerals nexus signal could lead to structural transformations in resource governance, potentially forcing industry and government actors to adopt integrated resource management models. Capital allocation may increasingly favor projects with embedded water-efficient technologies or located in lower water-risk areas. Regulatory frameworks could mandate combined water-mineral exploitation assessments, elevating water stress into mainstream resource policy discourse.

This is not merely incremental environmental management but a systemic shift recognizing water scarcity not as a side risk but a foundational constraint in resource extraction. However, some may interpret water risks as surmountable through technological innovation or alternate sourcing, potentially underestimating systemic hydrological limits.

While water-saving efforts in agriculture signal broad applicability of efficiency technologies, the complexity and scale of applying equivalent principles in mining remain a competitive frontier that may fragment or consolidate industrial ecosystems, depending on regulatory and capital market responses.

Early Indicators to Monitor

- Rise in ESG disclosures explicitly integrating water use and scarcity metrics in critical mineral extraction and processing.

- Increased R&D and patent filings in water recycling and water-efficient extraction technologies for mining sectors.

- Emergence of regional regulatory drafts combining water and mineral resource governance or integrated resource risk assessments.

- Shifts in financial institution capital allocation strategies favoring projects with joint water-mineral risk mitigation strategies.

- Clustering of industry conferences, public-private partnerships, and standards bodies focusing on the water-energy-minerals nexus.

Disconfirming Signals

- Widespread adoption of alternative mineral sourcing or synthetic substitutes nullifying water-intensive extraction in vulnerable regions.

- Breakthrough technologies significantly decoupling water use from mineral extraction at scale.

- Lack of integration of water risk in government or industry supply chain policies over the next decade.

- Significant geopolitical or economic shocks deprioritizing environmental resource governance frameworks.

Strategic Questions

- How can capital deployment strategies incorporate water scarcity footprints alongside mineral supply considerations to future-proof investments?

- What governance innovations are needed to regulate and incentivize integrated water-mineral resource stewardship in critical supply chains?

Keywords

Water Scarcity; Critical Minerals; Supply Chain Resilience; Resource Governance; ESG Disclosure; Water-Energy Nexus; Industrial Adaptation

Bibliography

- Securing Critical Minerals at Scale: Multilateral Solutions for Energy, Defense, and Semiconductor Supply Chains. ORF Online. Published 04/03/2026.

- The UK will invest £50 mn to boost domestic production of critical minerals, in a bid to reduce reliance on increasingly pressurised global supply chains. Emperor Works. Published 02/07/2026.

- Measuring the amount of water stress is important for understanding water risk in environments around the world. ClimateCheck. Published 11/01/2026.

- Water-saving and irrigation technology: In response to water scarcity, Kazakhstan introduced water-saving systems on over 158,000 hectares in 2024, with subsidies and targets to expand coverage to 1.3 million hectares by 2030. Trade.gov. Published 15/11/2025.

- The SAIMM Conference will convene governments, industry leaders, financiers, researchers, and civil society to chart pathways from extraction to value addition, ensuring Africa captures prosperity across the full critical minerals value chain. SAIMM. Published 23/02/2026.