The Emergence of Stablecoin-Centric Local Payment Ecosystems as a Structural Inflection in Decentralised Finance

The future of tokenised and decentralised finance (DeFi) is commonly framed around innovation in asset tokenisation, cross-chain interoperability, and central bank digital currencies (CBDCs). While these areas have significant visibility, a less recognised yet structurally consequential development is the embedding of stablecoins—not merely as trading intermediaries but as foundational elements in local payment networks and merchant tools through ubiquitous interfaces like QR codes and global wallets. This signal points toward the gradual construction of parallel, stablecoin-based transactional ecosystems that may reshape capital allocation, regulatory frameworks, and industry structures over the next decade.

Signal Identification

This development qualifies as an emerging inflection because it marks a shift from stablecoins functioning mainly within crypto markets towards direct integration with everyday payment infrastructure and merchant adoption. It is currently nascent but plausible to scale within 5–10 years, supported by expanding payment volume forecasts and growing acceptance in commercial environments. The plausibility band is medium to high, as stablecoins such as USDT and USDC already process substantial transactional volumes, and technical enablers like QR code integration and global wallets are widely accessible. The primary sectors exposed include financial services (payments and remittances), retail and merchant services, regulatory environments defining money transmission, and banking.

What Is Changing

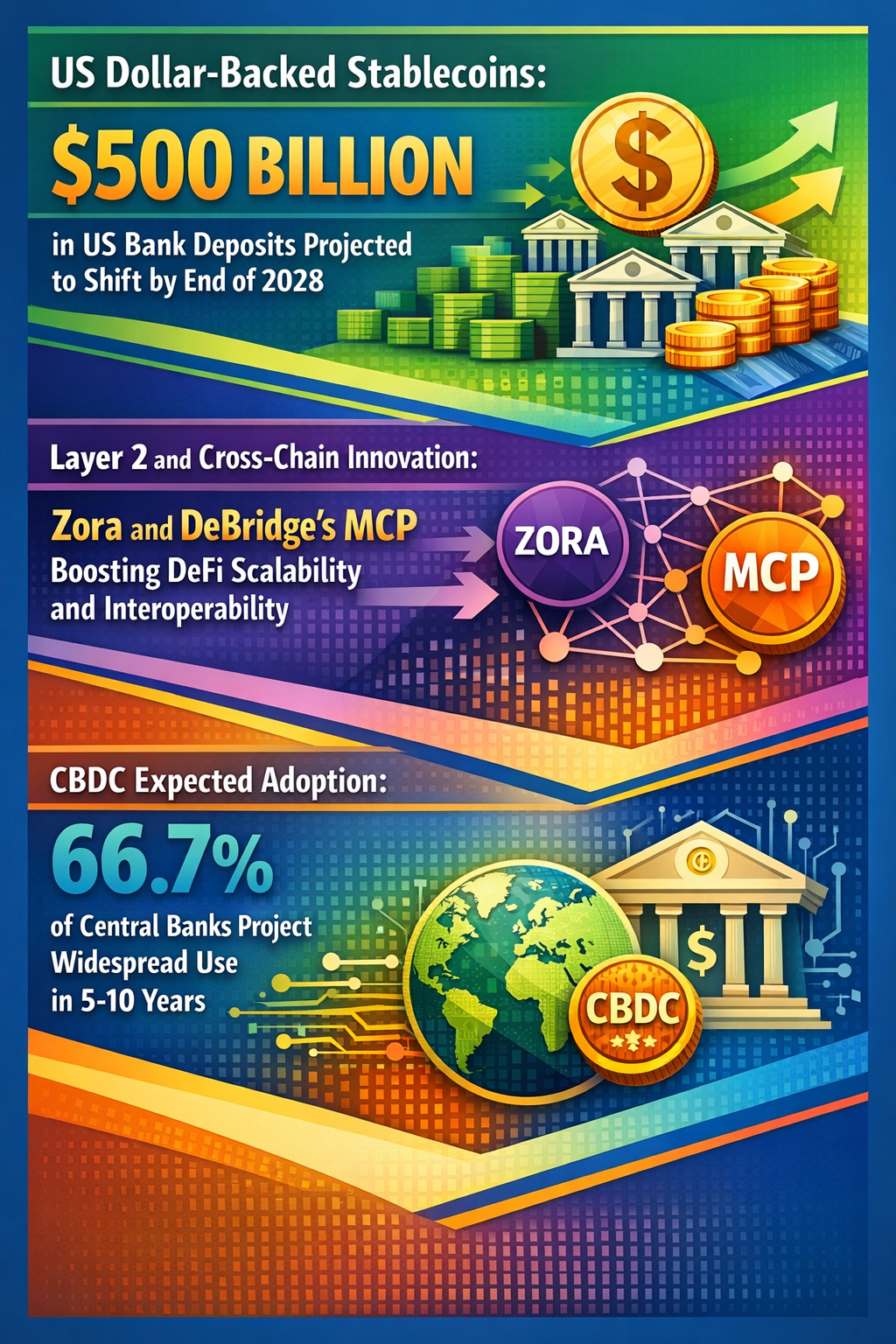

First, stablecoins have traditionally been positioned as tools for crypto trading and liquidity management. However, recent advances show stablecoins embedding themselves directly into payment networks, as indicated by the integration of stablecoins into QR code payment systems, global wallets, and card products enabling seamless merchant transactions (MEXC 2026). This is a structural change that transitions stablecoins from backend liquidity instruments to frontend transactional money substitutes.

Second, payment volume forecasts signal growth to as much as $50 trillion annually by 2030 through stablecoins (CryptoBriefing 2026). This scale exceeds mere trading activity and approaches traditional payment rails’ volumes, suggesting a reallocation of economic activity from fiat and card-based systems to algorithmically governed crypto-based instruments.

Third, central banks focus on CBDCs as digital money with two-thirds of institutions forecasting adoption within 5 to 10 years (CentralBanking 2026). Yet, stablecoins issued by regulated intermediaries may form a parallel, privately governed digital currency layer that interacts with or even competes against CBDCs in consumption and transaction environments, particularly in cross-border payments.

Finally, the reported withdrawal of approximately $500 billion in deposits from U.S. banks toward dollar-backed stablecoins by 2028 (Reuters, 2026) highlights potential disintermediation of traditional financial institutions. This partial reallocation could trigger liquidity pressures and regulatory scrutiny, motivating banks and regulators to reconsider capital allocation and oversight frameworks.

Disruption Pathway

The stablecoin-enabled local payment ecosystem is likely to evolve through a sequence of amplifying conditions. Initially, stablecoin payments will gain traction in regions or sectors where banking access is limited, payment costs are high, or remittance flows are significant. Merchant adoption will accelerate as stablecoin-based digital wallets offer cost and efficiency advantages over legacy card systems, facilitated by user-friendly integration of QR codes and global wallets.

As transaction volumes grow, stablecoins will begin to siphon off retail transactional revenue from banks, card networks, and payment processors. This disintermediation will stress traditional payment infrastructure and may compel incumbent banks to increase fees or restrict services, further pushing consumers and merchants toward stablecoins. Concurrently, regulators faced with potential financial instability risks due to stablecoin issuer concentration and regulatory arbitrage will impose new oversight requirements, potentially reshaping the operational and capital models for stablecoin issuers and custodians.

The interplay between CBDCs and stablecoin ecosystems will further complicate regulatory and systemic responses. Should CBDCs fail to offer the same convenience, privacy, or cost benefits, stablecoins could entrench as preferred digital money for everyday transactions. Conversely, CBDCs might integrate stablecoin functionality or enforce interoperability standards, driving convergence.

Over a decade, these dynamics may cause a bifurcation in the financial landscape: a parallel, decentralised, stablecoin-dominated retail payment system will coexist with (or partially supplant) traditional bank-based payment rails. This shift would challenge the monopoly of banks over retail money creation and transmission, potentially recalibrating capital flows, risk governance, and monetary policy transmission mechanisms. Payment rails may become multichain, tokenised, and interoperable by default, with stablecoins as the primary transactional unit.

Why This Matters

For capital allocators, this evolving payment landscape may dictate strategic deployment of resources into stablecoin infrastructure, merchant services, and interoperability solutions, hedging against declining returns in traditional payments. Regulatory bodies will need to anticipate the emerging systemic risks from large-scale stablecoin usage, such as concentration risk, anti-money laundering challenges, and financial stability threats, shaping policy frameworks that balance innovation with oversight.

Industrial positioning could be altered as technology firms, fintechs, and payments processors coalesce around stablecoin-enabled business models, potentially marginalising incumbent banks or forcing them into partnerships or reinvention. Supply chains for payment acceptance hardware and software will also shift toward blockchain-compatible ecosystems, requiring new standards and interfaces.

From a governance perspective, liability and consumer protection models will need to evolve to address the decentralized nature of stablecoins and their issuers. Payment disputes, fraud risk, and recourse mechanisms may require new legal and operational frameworks, particularly where cross-border transactions are prevalent.

Implications

This development may recalibrate capital flows away from traditional bank deposits toward stablecoin holdings, posing liquidity and funding challenges for banks. Regulatory frameworks could evolve toward stricter licensing and reserve requirements for stablecoin issuers, aligning them more closely to bank-like oversight or, alternatively, fostering a distinct regulatory category for digital transactional money.

Stablecoin-enabled payment systems might catalyse greater financial inclusion and cross-border remittance efficiency, but may also likely intensify regulatory fragmentation due to varying jurisdictional approaches to stablecoin governance. These developments should be distinguished from broad cryptocurrency hype; specifically, the focus here is on stablecoins as stitched into payment infrastructure rather than speculative assets.

Competing interpretations may view CBDCs as the dominant future payment method rendering stablecoins redundant; however, the decentralised governance and private innovation advantages stablecoins provide could resist such overtaking, at least in certain geographies or market segments.

Early Indicators to Monitor

- Volume growth of stablecoin transactions in retail and cross-border payment contexts, particularly merchant-acceptance metrics.

- Expansion and adoption of stablecoin payment integrations such as QR code protocols and global wallet deployments.

- Regulatory proposals and enacted frameworks specifically targeting stablecoin issuers as payment system infrastructures rather than trading intermediaries.

- Changes in bank deposit flows related to stablecoin issuance growth, especially dollar-backed stablecoins.

- Merchant onboarding rates to stablecoin payment tools and partnerships between fintechs and stablecoin issuers.

Disconfirming Signals

- Lack of meaningful merchant adoption or user uptake of stablecoin payment methods over a multi-year horizon.

- Regulatory crackdowns or prohibitions limiting stablecoin issuance, convertibility, or payment use cases.

- Successful widespread launch and rapid adoption of CBDCs that fully replicate stablecoin benefits, crowding out private stablecoins.

- Technological or security failures causing loss of user trust in stablecoin payment mechanisms.

- Persistently stable or increasing deposit bases within banks without corresponding shifts toward stablecoins.

Strategic Questions

- How should capital allocation strategies adapt in anticipation of a bifurcated payment ecosystem where stablecoins capture significant transactional volumes?

- What regulatory models could effectively govern stablecoin payment systems to balance innovation, consumer protection, and systemic risk?

- How will incumbent financial institutions need to reposition themselves to remain competitive as stablecoins facilitate direct merchant payments?

- What standards and interoperability protocols are critical to enable scalable cross-chain and cross-jurisdictional stablecoin payment networks?

- Which partnerships or ecosystem investments could position governments or firms favorably in the evolving stablecoin-dominated payment infrastructure?

Keywords

Stablecoins; Decentralised Finance; Central Bank Digital Currency; Payment Networks; Financial Inclusion; Regulatory Frameworks; Liquidity Disintermediation; Tokenisation; Cross-Chain Payments.

Bibliography

- MEXC 2026 – Stablecoins embedding into local payment networks through QR codes and card integration.

- CryptoBriefing 2026 – Stablecoins projected to process $50 trillion in payments by 2030.

- CentralBanking 2026 – Majority of central banks anticipate CBDC adoption in next 5–10 years.

- Reuters/WealthProfessional 2026 – Dollar-backed stablecoins may attract $500bn in deposits away from banks by 2028.