Within the domain of China’s evolving strategic, technological, and geopolitical landscape, a set of subtle, weak signals has emerged pointing to early-stage but potentially disruptive shifts. These signals range from China transitioning to AI innovation leadership, fluctuating global scientific influence, to nuanced Sino-Russian high-tech cooperation challenging current security paradigms. Though fragmented and nascent, these indicators suggest possible divergences from established assumptions of China as a technology follower and highlight shifting global innovation and geopolitical balances.

The uncertainty lies in the pace, scale, and concrete outcomes of these signals, as well as counter-forces from U.S., Japan, and European responses. Capturing these weak signals allows for anticipation of latent opportunities or creeping risks that could significantly reshape global market dynamics, supply chains, and strategic competition over the next decade.

| Weak Signal Name | Description | Visibility / Maturity | Direction of Travel | Why it Matters |

|---|---|---|---|---|

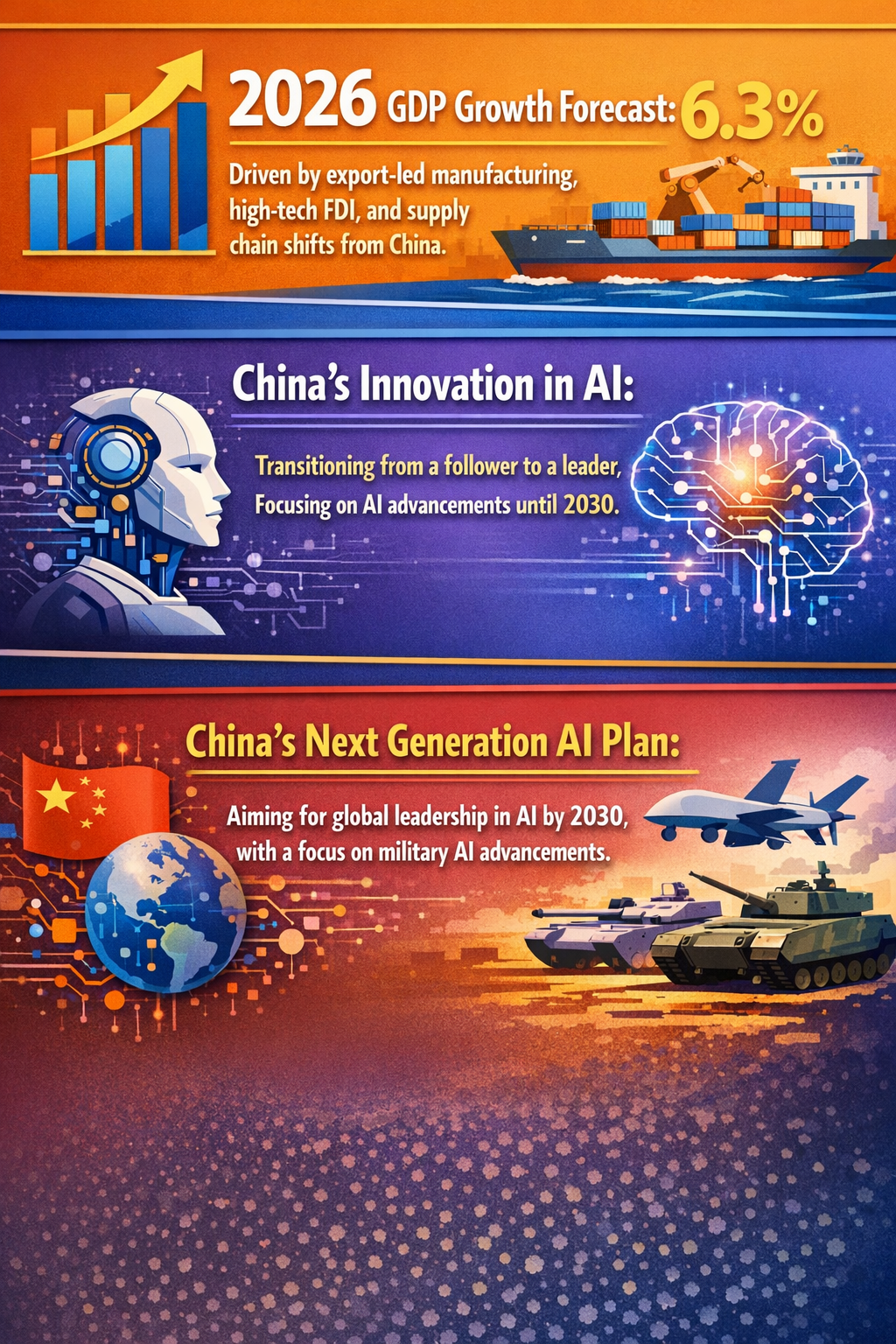

| China’s Leap from AI Catch-Up to Innovation Leader | China’s 5-year plan prioritizes breakthroughs in AI and other frontier technologies, moving beyond just catching up with the U.S. | Early-adopter only; fragmented indicators from policy and R&D expansions | Emerging | Challenges the long-held assumption that China trails U.S. in AI; could shift global tech leadership and related economic influence (WHEC). |

| Fluctuating US Scientific Convening Power | Domestic constraints on US research publishing and funding risk ceding global science leadership as China and allies boost R&D output and infrastructure. | Isolated and fragmented policy signals in US science management | Volatile | Could reorient global innovation networks and intellectual leadership, influencing global norms and technological agenda-setting (Food Ingredients First). |

| Emerging Sino-Russian High-Tech Military Cooperation | Joint development in space and advanced weapons tech indicates a growing strategic partnership that could affect geopolitical stability. | Niche diplomatic and military references; early-stage tech collaboration | Emerging | Signals potential new axis in strategic military balance; could disrupt prevailing security frameworks (USCC). |

| China’s Commercialization of Sodium-Ion Batteries | China is commercializing clean-energy battery tech (sodium-ion) that requires fewer critical raw materials, diverging from dependency on scarce minerals. | Early commercialization but niche market presence | Emerging | Potential to reduce reliance on critical mineral supply chains, altering geopolitical leverage in resource-scarce domains (Carnegie Endowment). |

| Japan's Intensified Export Controls & R&D Focus on Critical Minerals | Japan is fortifying its supply chains and tech advantages through strategic controls and investment to counterbalance China’s advances. | Policy drafts and announcements; limited cross-sector uptake so far | Emerging | Reflects escalating resource contestation and technological rivalry in East Asia, influencing investment and trade flows (Foreign Affairs). |

| Shifting Economic Growth Drivers with Supply Chain Relocation | Projected GDP growth partly relies on supply chain relocation away from China, paired with increasing high-tech foreign direct investment inflows into China. | Projections based on current trade and FDI data; fragmented | Volatile | Undermines the narrative of unchecked Chinese industrial dominance; implies complex regionalization of manufacturing (KBA13). |

| US Science & Tech Investment Decline | US reducing resources in key S&T domains at a time when China is accelerating, especially in emerging tech areas. | Isolated policy and funding trends; risk of volatility remains | Dormant/Volatile | Indicates creeping risk of US technological decline, which may affect global innovation and competitiveness (The National Interest). |

Two key proto-pattern clusters emerge from these weak signals:

First, Technological Leadership Transition and Ecosystem Realignment: China’s advancing AI ambitions combined with commercialization of resource-light battery tech, alongside waning U.S. leadership in science publishing and research funding, hint at an incipient global innovation reordering. This reordering is still fragmented and competitive, with Japan and Europe seeking to reinforce their critical mineral strategies and clean tech capabilities. If these signals converge, they could mark a shift from a U.S.-centric innovation order to a multipolar system with China as a co-leader, triggering supply chain, investment, and market disruptions globally.

Second, Strategic-Military-Tech Cooperation Challenge: The Sino-Russian push into joint high-tech weapon development and space technologies signals a nascent but volatile shift in geopolitical competition. This cluster encompasses moves away from traditional Western controls over emerging dual-use tech and could accelerate arms races or strategic instability, with unpredictable systemic implications for global security.

Rapid Breakthrough in Sino-Russian Next-Generation Military Technology

Wild Card – Disruptive Risk

Very High

Unexpected acceleration in military tech cooperation could catapult China-Russia into a leading position disrupting global strategic stability.

This risk deserves close monitoring due to its capacity to rapidly undermine established deterrence frameworks and trigger cascading geopolitical tensions.

China Emerges as a Global AI Standard-Setter, Undermining Western Tech Governance

Wild Card – Disruptive Opportunity

High

China unexpectedly leads in AI innovation governance frameworks and exports its standards globally, reshaping trade and technology ecosystems.

This scenario presents a strategic opportunity to lead in shaping the future AI-enabled economic order, with implications for markets, intellectual property, and data governance.

Massive Supply Chain Disruption from Sudden Shift Away from China in Critical Battery Technologies

Wild Card – Disruptive Risk

High

A rapid, large-scale pivot by major economies to South Korean or Japanese battery technology producers could burden China’s manufacturing base and global supply chains.

While difficult to predict, this shift could unexpectedly disrupt global clean energy value chains and cause market volatility affecting multiple sectors.

Preparedness should emphasize tracking niche indicators and fostering adaptive strategies that can respond to fragmented but directional signals rather than relying solely on dominant trend extrapolation.